How many bank accounts does the average person have? 2026

+1 more

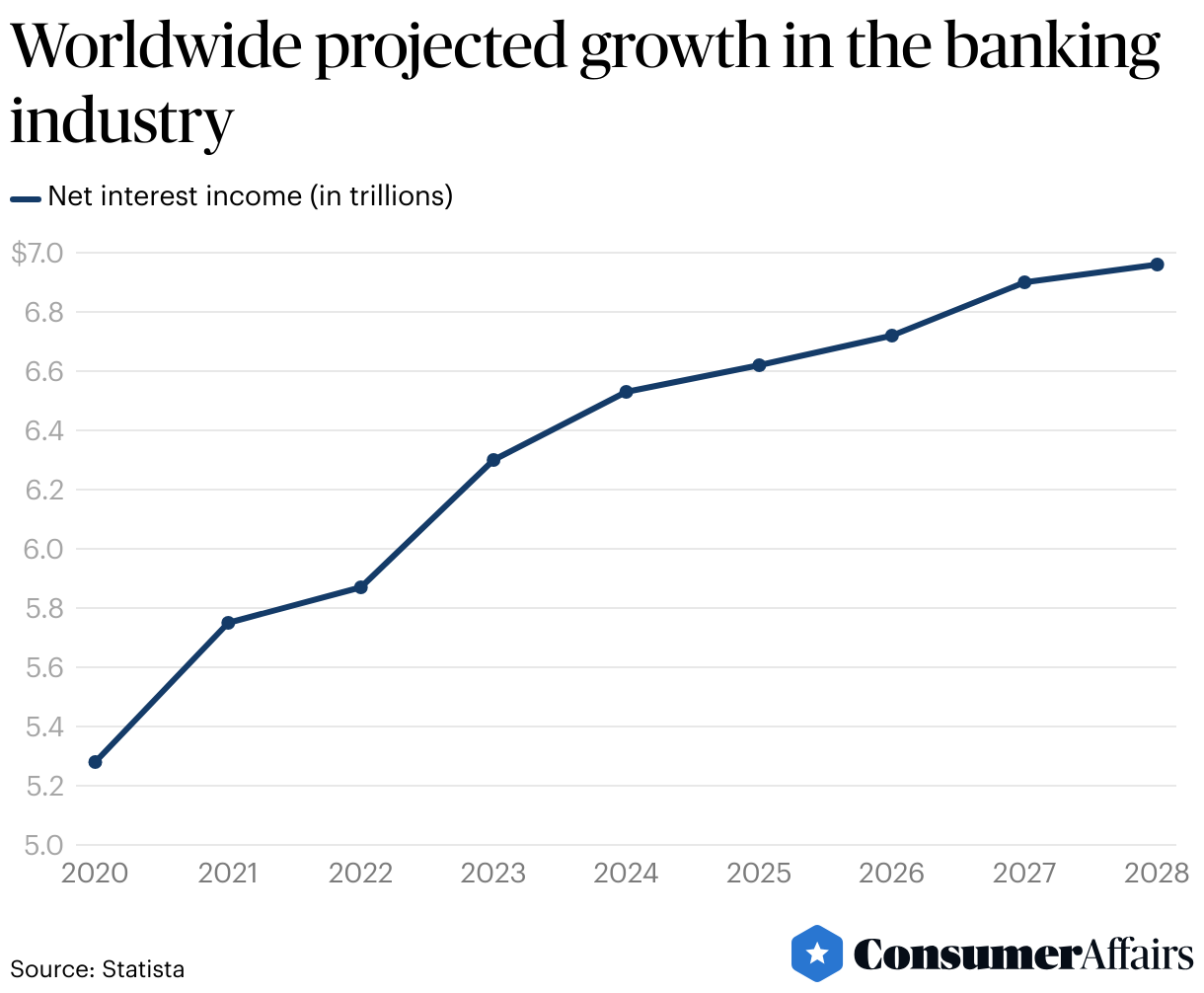

Almost every household in the U.S. has access to at least one bank account. However, household income is an increasingly significant factor for those households without an account. Globally, the number of adults with at least one bank account is projected to exceed 80% for the first time in 2024. Both the number of adults with access to a bank account and net profits in the banking industry are projected to continue to grow throughout the rest of the decade.

Consumers in the U.S. had an average of 5.3 different accounts across financial institutions in 2019.

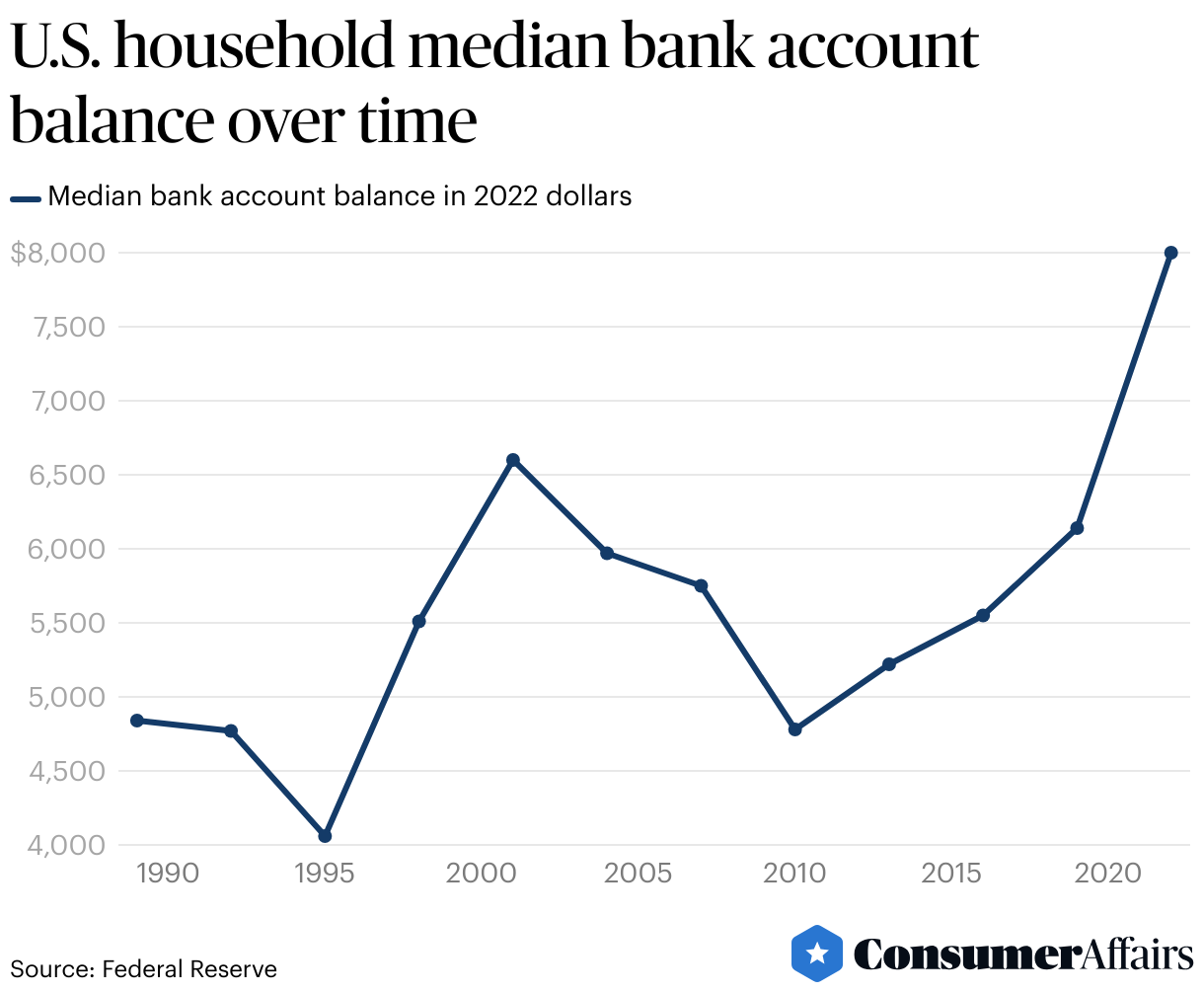

Jump to insightThe median household bank account balance in the U.S. climbed to $8,000 in 2022.

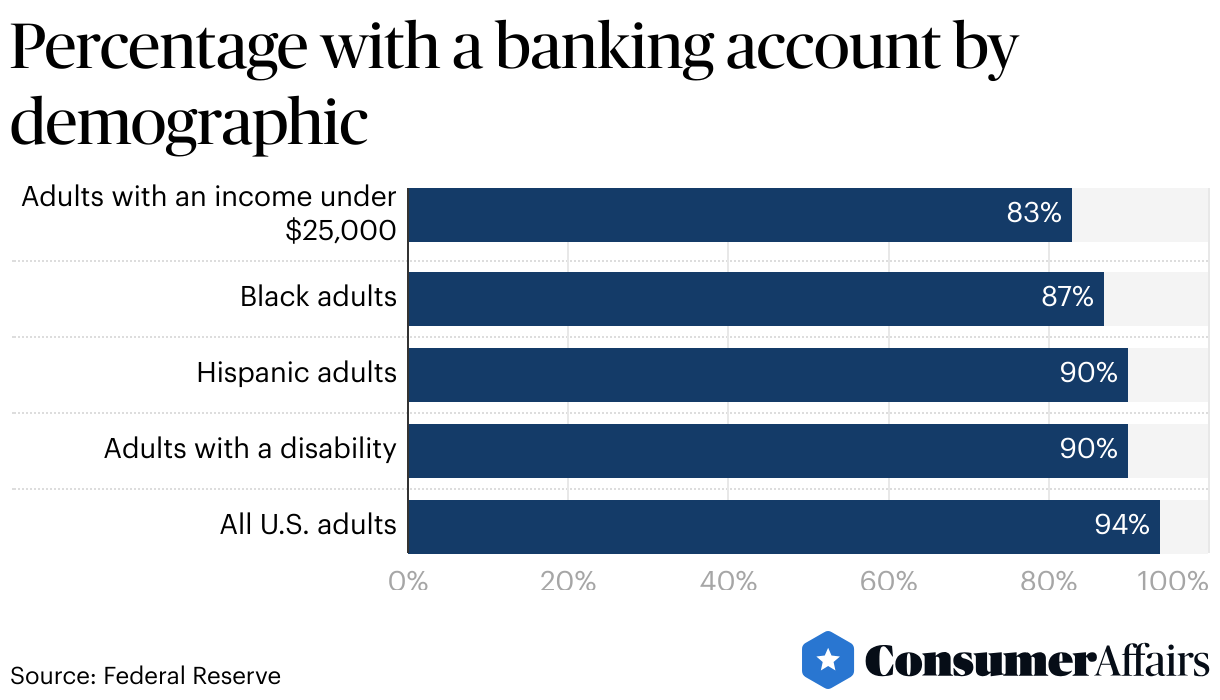

Jump to insightBetween 94% and 95.5% of U.S. households have access to at least one bank account. That number decreases to 83% for households with a family income below $25,000.

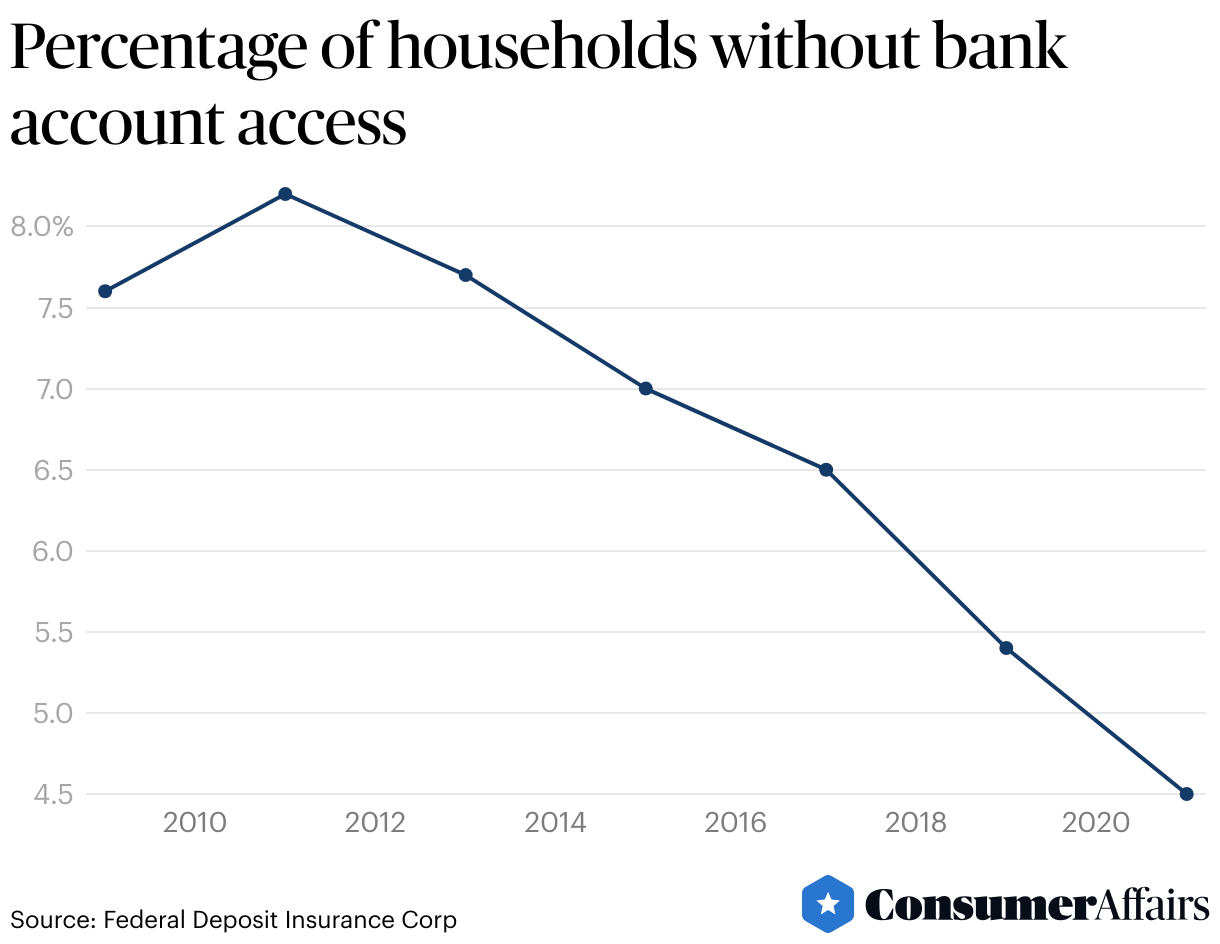

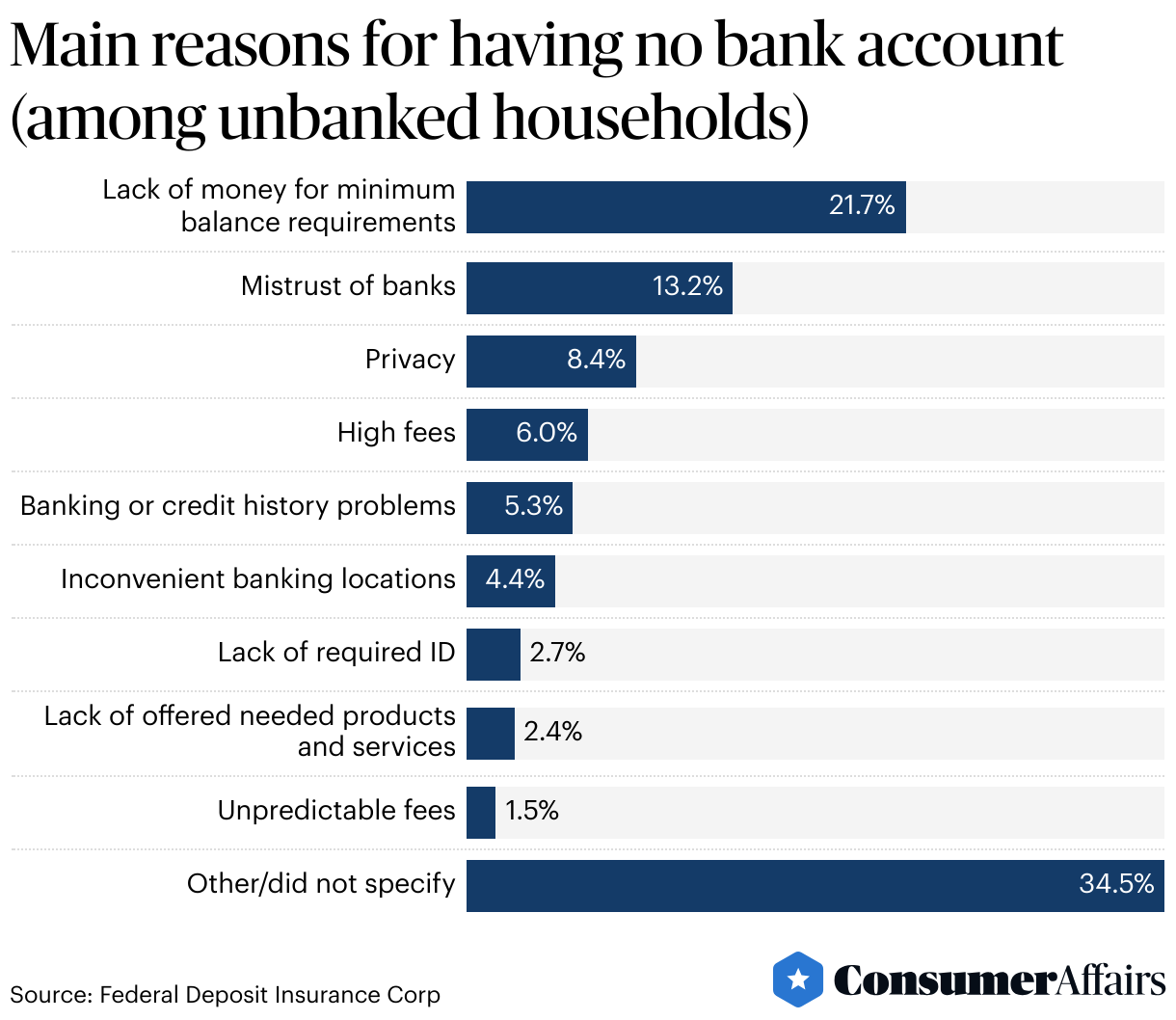

Jump to insightFor households without banking accounts, lack of money to meet minimum balance requirements was the most common reason for not having one in 2021.

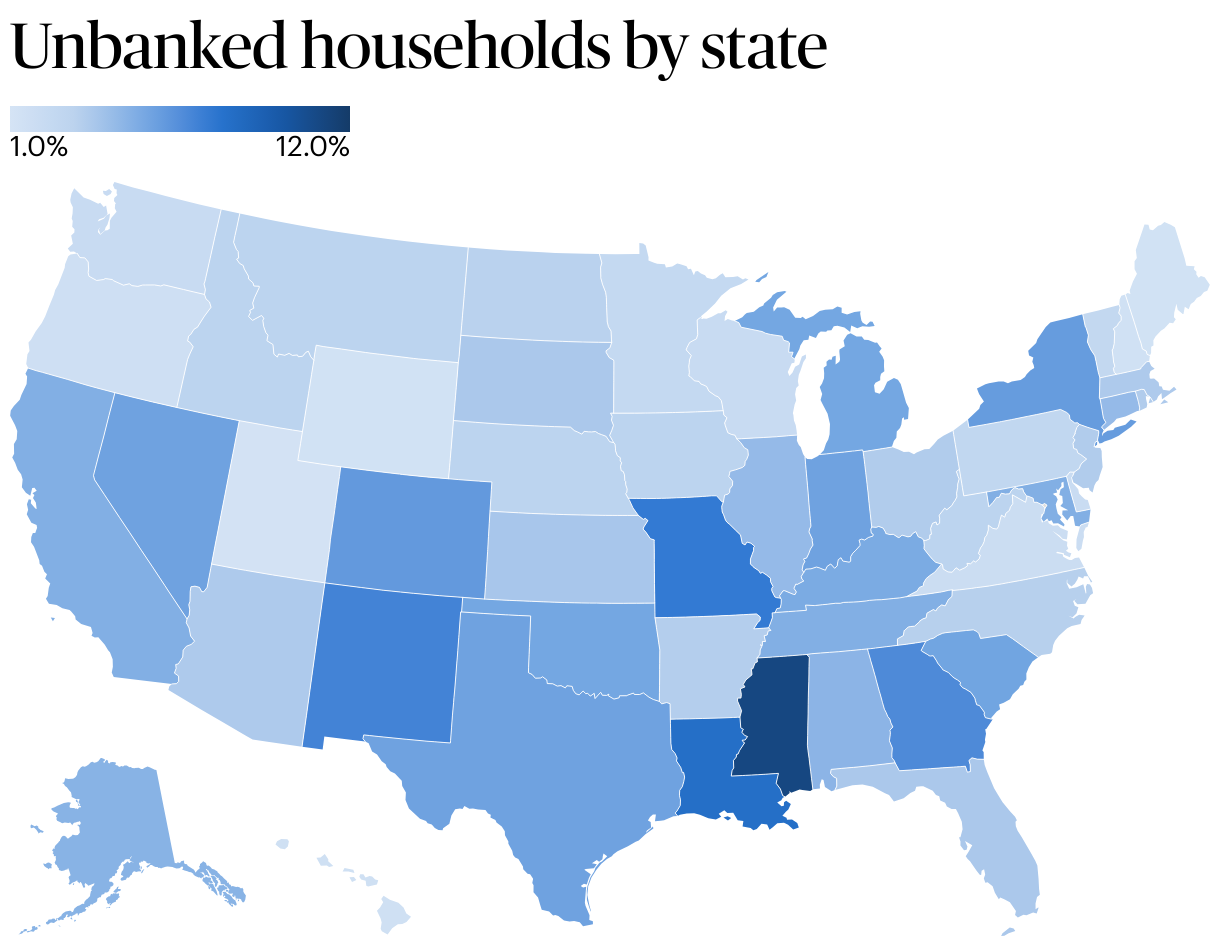

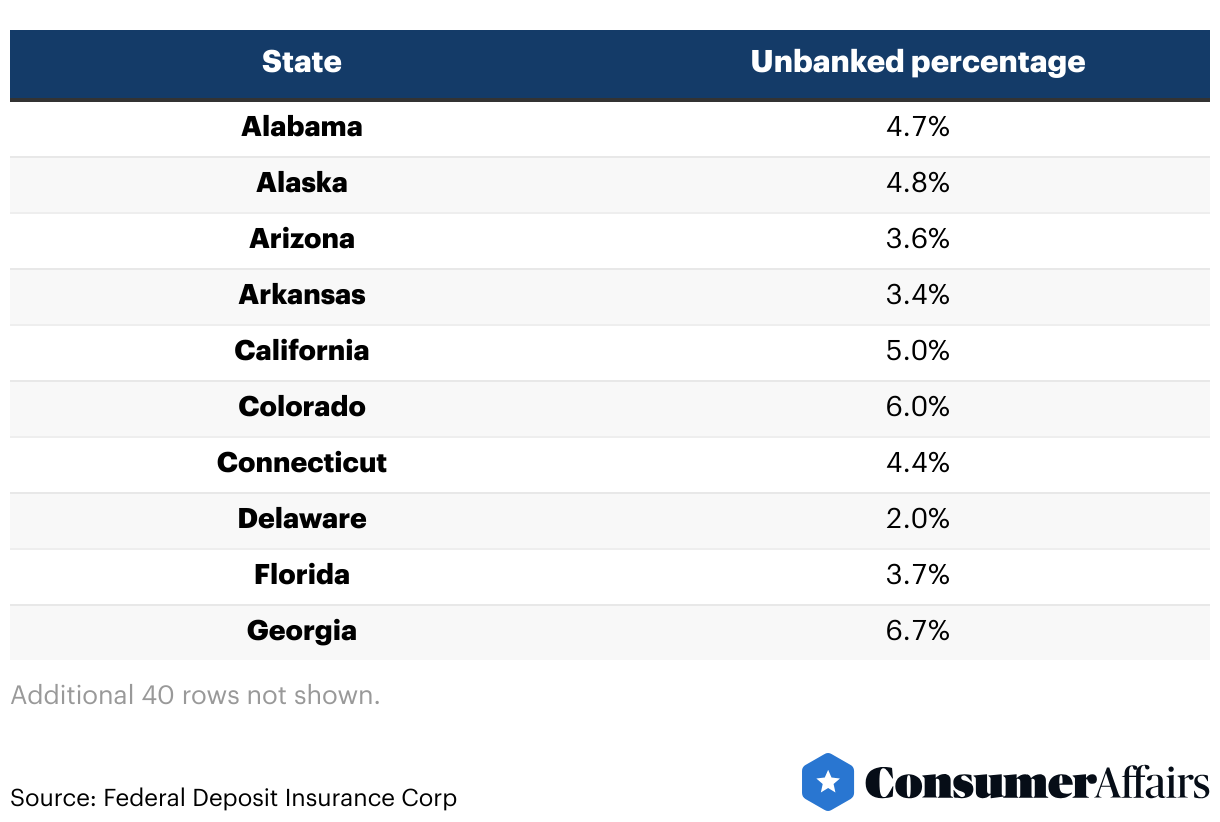

Jump to insightThe number of households with no bank account varies significantly across the U.S. Mississippi has the highest percentage of households without bank accounts (11.1%), while Utah has the lowest (1.2%).

Jump to insightGeneral bank account statistics

According to a survey published in 2019, the average consumer in the U.S. has a total of 5.3 accounts across financial institutions. The share of households without access to at least one banking account has decreased consistently since 2011.

The median bank account balance for a family in the U.S. was $8,000 in 2022. That figure has climbed significantly in the past 30-plus years, even when adjusted for inflation.

Bank account owner demographics

The rates of bank account ownership vary among demographic groups. Racial minorities, people with lower incomes and people with disabilities are all less likely than the general public to have a bank account.

Unbanked rate vs. underbanked rate

The term “unbanked” refers to adults who don’t have a transaction account (a checking, savings or money market account) and also don’t have a spouse or partner with such an account. As noted in the table above, unbanked rates are highest among people with the lowest incomes.

The Federal Deposit Insurance Corp. (FDIC) also tracks the number of “underbanked” households. This describes households that had a checking or savings account but still needed to use nonbank financial products, like check cashing, rent-to-own or tax refund anticipation services, at some point in the last year. In 2021, 14.1%, or approximately 18.7 million U.S. households, qualified as underbanked.

Unbanked households by state

As a region, the South has a higher rate of unbanked households than other parts of the country.

The percentage of unbanked households in the South tallied 4.9% in 2021, compared to 4.2% in the West and Midwest regions and 4.1% in the Northeast. Among states, Mississippi had the highest percentage of unbanked households, with 11.1%, while Utah had the lowest at 1.2%.

Reasons people are unbanked

The FDIC’s National Survey of Unbanked and Underbanked Households provides insights into the reasons why unbanked households are disconnected from the banking system. The chart below details these households’ stated primary reasons.

Banking industry projections

Globally, the World Bank estimates that 76% of adults have access to a bank account. Bank account ownership increased by 50% between 2011 and 2021, with developing economies serving as the primary driver of that growth.

Banking industry profits have continued to rise as well. The projected net interest income (the primary revenue source for most banks) of the industry is forecast to reach $6.5 trillion in 2024. Growth of net interest income is expected to continue at an annual growth rate of 1.57% through 2028.

FAQ

What percentage of the U.S. population has a bank account?

Between 94% and 95.5% of adults in the U.S. have access to a transaction account, defined as a checking, savings or money market account. A person is considered to have access to an account if they own the account or if it is owned by their partner or spouse.

How much does the average American have in their bank account?

According to data collected by the Federal Reserve, the median bank account balance in the U.S. was $8,000 in 2022. Even adjusting for inflation, this balance is higher than it has been since the Federal Reserve began collecting data on bank balances in 1989.

Who is least likely to have a bank account in the U.S.?

People with incomes below $25,000 per year, racial minorities and adults with disabilities are less likely than the general population to have a bank account. Geographically, residents of Mississippi and Louisiana have significantly lower rates of bank account ownership than the national average.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Mercator Advisory Group/Javelin Strategy, “ATM Banking: It’s Not Just About Cash Withdrawal Anymore.” Accessed Mar. 9, 2024.

- Statista, “Banking - Worldwide.” Accessed Mar. 10, 2024.

- Board of Governors of the Federal Reserve, “Survey of Consumer Finances.” Accessed Mar. 9, 2024.

- Board of Governors of the Federal Reserve, “Report on the Economic Well-Being of US Households in 2022 – May 2023.” Accessed Mar. 9, 2024.

- Federal Deposit Insurance Corp., “FDIC National Survey of Unbanked and Underbanked Households.” Accessed Mar. 9, 2024.

- Federal Deposit Insurance Corp., “Unbanked Rates by Geography – 2021.” Accessed Mar. 9, 2024.

- World Bank Group, “The Global Findex Database.” Accessed Mar. 26, 2024.

Figures